Following the post-pandemic catch-up phase, the air market is entering a more constrained period, where demand continues to grow but at a more predictable pace. Concurrently, industrial tensions persist, limiting airlines’ adjustment margins. In this context, the intermediate segment of 120 to 150-seat jet airliners (often referred to as extended “regional jets” or small narrowbodies) is once again emerging as a precise network management tool, particularly in fragmented, multi-market areas like the Caribbean and Latin America.

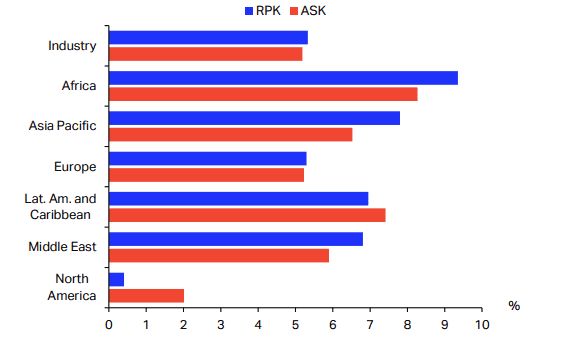

In 2025, global passenger traffic grew by 5.3% in terms of revenue passenger kilometers (RPK), a more moderate increase than the previous year, according to the passenger air transport market analysis published by IATA in December 2025. This normalization does not indicate a weakening of demand, but rather a return to historical rates after the shock of 2022-2024. The signal is clear: demand is present, but supply remains constrained.

In the Latin America and Caribbean region, the dynamic remains above the global average. Traffic there grew by nearly 7% in 2025, driven by both the recovery of international flows and strong domestic markets, primarily Brazil, where domestic traffic surged by over 11% during the year, according to the same IATA data. This sustained growth exerts direct pressure on fleets and capacity choices.

Real Demand, But Aircraft Still Delayed

While passengers are present, aircraft are arriving more slowly. In 2025, global capacity (ASK) grew by only 5.2%, slightly below demand, pushing the load factor to a record high of 83.6%, the highest ever recorded for a full year. For airlines, this figure is a double-edged sword: it demonstrates good capacity discipline, but also a persistent lack of operational flexibility.

Willie Walsh, IATA Director General, summarized it bluntly in January 2026: aerospace supply chain difficulties were “the main headache for airlines in 2025,” including delivery delays, engine unavailability, and maintenance pressures, with an estimated additional cost of over $11 billion for the sector. For lack of better options, operators extended the lifespan of existing aircraft and maximized load factors, an effective short-term solution, but one that is difficult to sustain.

It is in this context that the ramp-up announced by Embraer takes on its full meaning for regional markets.

This tension between traffic growth and struggling capacity is clearly evident in the regional data published by IATA for 2025.

RPK vs. ASK Evolution by Region (2025) – Source: IATA Sustainability and Economics, IATA Information and Data – Monthly Statistics

Embraer: Industrial Visibility and the Return of the Intermediate Segment

In early 2026, the Brazilian manufacturer confirmed its intention to gradually increase its production of commercial jets, driven by a growing E2 order book and a gradual, though still incomplete, improvement in the supply chain. Statements relayed by Reuters emphasize a key point for airlines: industrial stabilization would only be fully achieved by 2026, but visibility is already improving.

This caution is reflected in the group’s official financial documents. In its annual report (Form 20-F), Embraer acknowledges its continued strong dependence on a limited number of critical suppliers, with component purchases representing over 77% of its commercial aviation production costs in 2024. The manufacturer also highlights that supply chain delays or failures could still affect production rates and delivery schedules, a point that airlines must integrate into their fleet decisions.

But despite these constraints, the message is clear: the segment up to 150 seats, the core of the E-Jets E2 family, is among the group’s industrial priorities, precisely because it meets structural demand in regional markets.

Why the 120–150 Seat Segment Is Particularly Suited to the Caribbean and Latin America

In the Caribbean and Latin America, the challenge is not so much creating demand as serving it correctly. Many inter-island routes or connections between secondary cities and regional hubs show sufficient volumes to be viable, but insufficient to absorb 180 to 220-seat single-aisle aircraft without degrading load factors.

In the Caribbean, where most air routes remain low-density, the 120-seat aircraft is less a standard than an operational ceiling, relevant only on clearly identified routes with strong seasonal demand.

The 120 to 150-seat aircraft then becomes a precision tool. It allows for increased frequencies, smoothing out tourism seasonality, and opening up so-called “thin” routes with more controlled financial risk. This logic is all the more relevant given that traffic growth in the region is largely driven by international travel, which grew by over 7% in 2025, according to IATA’s analysis, while domestic markets remain highly contrasted from one country to another.

For airlines, the challenge is not just the cost per seat, but the ability to finely adapt supply to irregular flows, often dependent on tourism, diasporas, and regional connections. In this scenario, the intermediate segment plays a binding role between major hubs and secondary destinations.

Limits Well Identified by Operators

However, the rise of regional jets is not a miracle solution. Embraer’s financial documents remind us that delivery schedules remain exposed to industrial uncertainties, while access to financing remains a key factor, particularly in certain Caribbean markets where credit capacities remain limited.

Added to this are well-known operational constraints: maintenance slot availability, engine pressures, shortage of qualified personnel, and sometimes limited capacity of secondary airports to absorb an increase in frequencies. These are all parameters that require a coordinated approach between airlines, airport authorities, and regulators.

A Connectivity Lever, More Than an Industrial Bet

Ultimately, Embraer’s ramp-up should not be read as a mere industrial signal, but as an indicator of market rebalancing. In a phase where traffic growth is normalizing and capacity remains constrained, the 120 to 150-seat regional jet is once again a strategic tool for optimizing networks, rather than a default compromise.

For the Caribbean and Latin America, where regional connectivity directly conditions economic and tourism development, this segment offers a pragmatic response, provided its limitations are managed. The challenge for regional stakeholders will be less about following a trend than about intelligently integrating it into fleet, infrastructure, and financing strategies adapted to local realities.