From InterCaribbean (88% intra-regional capacity) to Arajet (86% extra-regional), Caribbean carriers embody divergent business models. The NACO/ACI-LAC study released in March 2026 maps a market whose fragmentation sheds light on the structural challenges facing the region’s airlines.

The Caribbean aviation market is served by a diverse mix of airlines, each with distinct business models and commercial strategies, reflecting the region’s inherent diversity in passenger segments. NACO’s report, commissioned by ACI-LAC, does not claim to be exhaustive but offers a selection of the most relevant players in 2025. Comparing their profiles sheds light on the market’s fragmentation and the strategic tensions running through it.

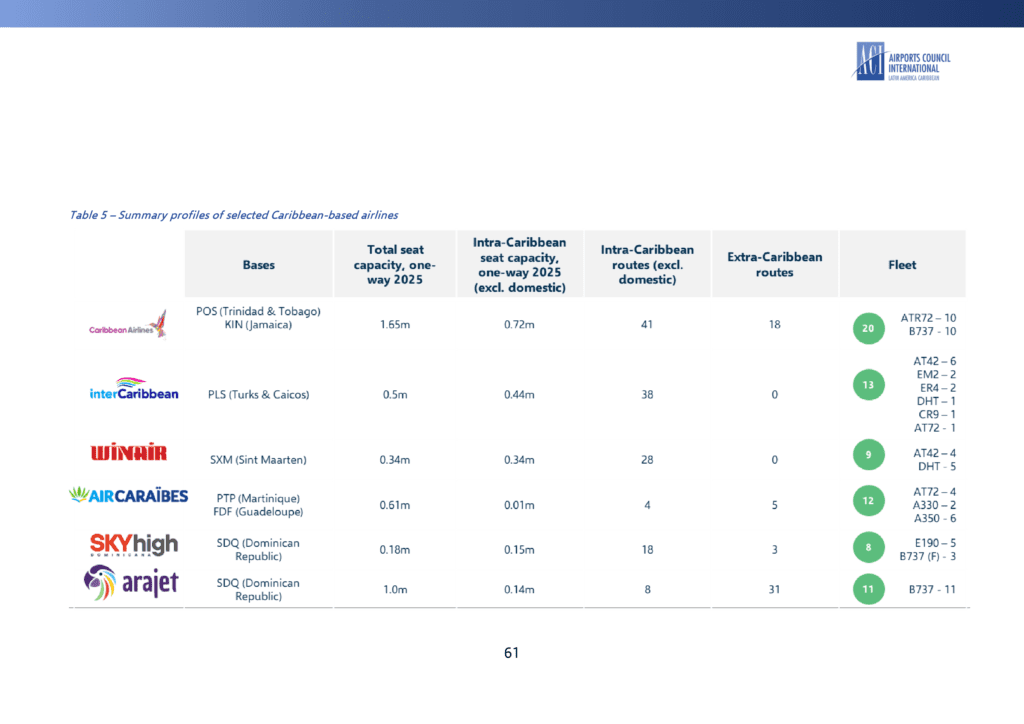

Summary profiles of selected Caribbean-based airlines: bases, total seat capacity 2025, intra-Caribbean capacity, intra and extra routes, fleet. Source: Cirium, NACO Analytics, NACO/ACI-LAC report, March 2026.

InterCaribbean Airways: the intra-regional bet

Headquartered in Providenciales (Turks and Caicos), InterCaribbean Airways deploys approximately 88% of its total seat capacity on the intra-Caribbean market in 2025. It also operates the highest number of intra-regional routes among Caribbean-based airlines. With hubs in Tortola and Barbados, the airline connects more than 20 destinations across 17 countries, operating a mixed fleet of turboprops and regional jets that balance operational needs between very short island hops and longer regional services. InterCaribbean illustrates a model whose strength is dense regional coverage, but which also bears the economic fragility inherent to Caribbean thin markets.

Caribbean Airlines: the dual-purpose flag carrier

Based in Port-of-Spain (Trinidad and Tobago) and Kingston (Jamaica), Caribbean Airlines positions itself as the region’s primary flag carrier. Its network extends beyond the Caribbean to North America (Fort Lauderdale, Miami, Orlando, Toronto). The airline uses predominantly the ATR 72-600 aircraft for short-haul intra-regional services and Boeing 737/737 MAX jets for longer routes, reflecting a dual focus on regional coverage and international reach — a distinctive feature compared to InterCaribbean. According to NACO, Caribbean Airlines has deployed approximately 44% of its total network seat capacity on the intra-Caribbean market in 2025.

Winair: the niche model

Winair, by comparison, deploys a niche-type business model. Based in Sint Maarten, the airline focuses mainly on short inter-island connections within the Leeward Islands (St. Barth, Saint Kitts and Nevis, Dominica, Saint Vincent and others), as well as the Dutch ABC islands (Aruba, Bonaire, Curaçao). With a small fleet of ATR 42 and de Havilland Twin Otters, Winair specialises in serving thinner markets with relatively frequent services. The NACO report illustrates, through this profile, the fragile but real viability of an ultra-specialised model for routes that low-cost models cannot economically serve.

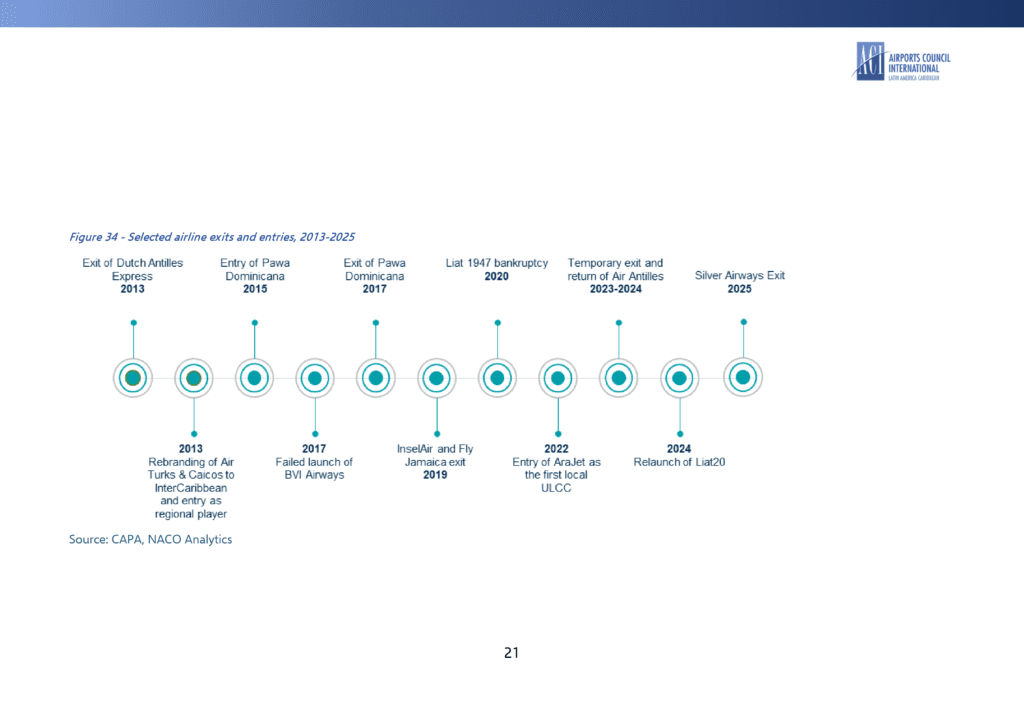

Timeline of selected airline entries and exits in the Caribbean, 2013-2025. A succession of failures (Pawa Dominicana, Fly Jamaica, InselAir, Silver Airways, Liat 1947) and entries (InterCaribbean, AraJet, Liat 2020). Source: CAPA, NACO Analytics, NACO/ACI-LAC report, March 2026.

Arajet and SKYhigh Dominicana: the new entrants

Emerging carriers based in the Dominican Republic — Arajet and SKYhigh Dominicana — represent another layer of market differentiation in recent years. Anchored in Santo Domingo (SDQ), Arajet has adopted an ultra-low-cost model with rapid expansion into the United States, Central America and South America, where the airline deployed 86% of its total seat capacity in 2025, with modest operations on intra-Caribbean routes. According to NACO, the carrier has grown more than tenfold since 2022, from roughly 100,000 seats (one-way) to more than 1 million in 2025. Capacity to North America has increased 18 times, from 20,000 seats in 2022 to 360,000 seats in 2024. Supported by an all-Boeing 737 MAX fleet, the airline competes head-to-head with established low-cost players including JetBlue, Frontier and Copa Airlines.

SKYhigh Dominicana, also based in Santo Domingo, remains more regionally focused, concentrating on scheduled and charter flights within the Caribbean market, with strategic expansion into North and South America. The airline uses mostly Embraer jets (E190), supplemented by Boeing 737s for all-cargo services, differentiating it from Arajet’s strictly passenger model. SKYhigh’s extra-Caribbean network focuses mainly on Miami while also operating tag flights between Santo Domingo and French Guiana via Martinique.

Foreign airlines: a structuring weight

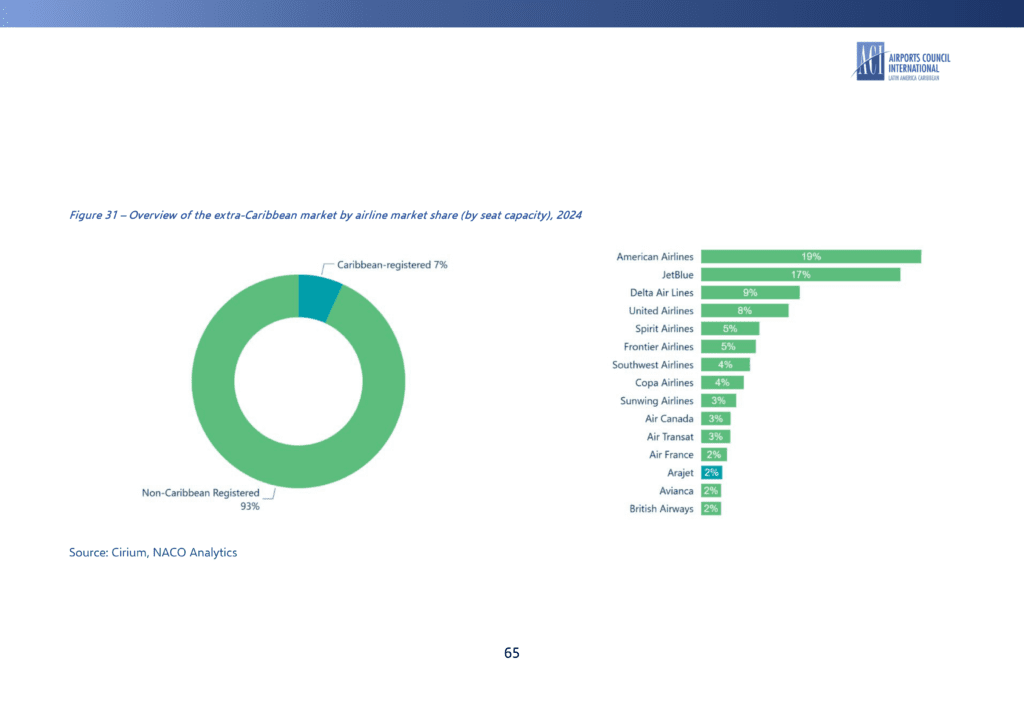

NACO’s report also documents the footprint of non-Caribbean airlines. Among foreign carriers, U.S.-registered JetBlue and Frontier operate several intra-Caribbean routes (predominantly to the Dominican Republic) from their base in Puerto Rico (SJU). Direct services originating from various U.S. airports add to this dispatch, with the major share of traffic to and from New York (JFK), Orlando (MCO), Boston (BOS) and Fort Lauderdale (FLL). European carriers (British Airways, KLM, Virgin Atlantic, TUI, Air France) operate tag and fifth-freedom routes to and from Europe. According to estimates reported by NACO, these European carriers represent roughly 10% of intra-regional seat capacity through tag operations.

The study also recalls a notable historical precedent: American Eagle, the regional brand of American Airlines, operated from Puerto Rico to the Virgin Islands, several Eastern Caribbean islands, Trinidad and Tobago, Haiti and St. Maarten, with a primarily turboprop fleet. In 2013, the carrier closed its Puerto Rican base as part of American Airlines’ Chapter 11 restructuring. Although Seaborne Airlines and JetBlue absorbed parts of the network, a noticeable connectivity gap remains to this day, reducing the efficiency and accessibility of intra-Caribbean air travel.

The weight of operational constraints

The diversity of models, however, does not offset a structural economic reality. According to the NACO study, Caribbean-based airlines — especially those operating intra-Caribbean routes — tend to rely on smaller aircraft types, with an average aircraft size of 47 seats per flight in 2025. Operating routes with relatively thin demand and short distances makes the unit cost of operations relatively high, as economies of scale are harder to achieve. Based on studies cited by NACO from IATA, Eurocontrol and the FAA, the estimated average operating unit cost of a 50-seater is roughly twice as high as the cost of a standard narrowbody (e.g. B737) per available seat kilometre.

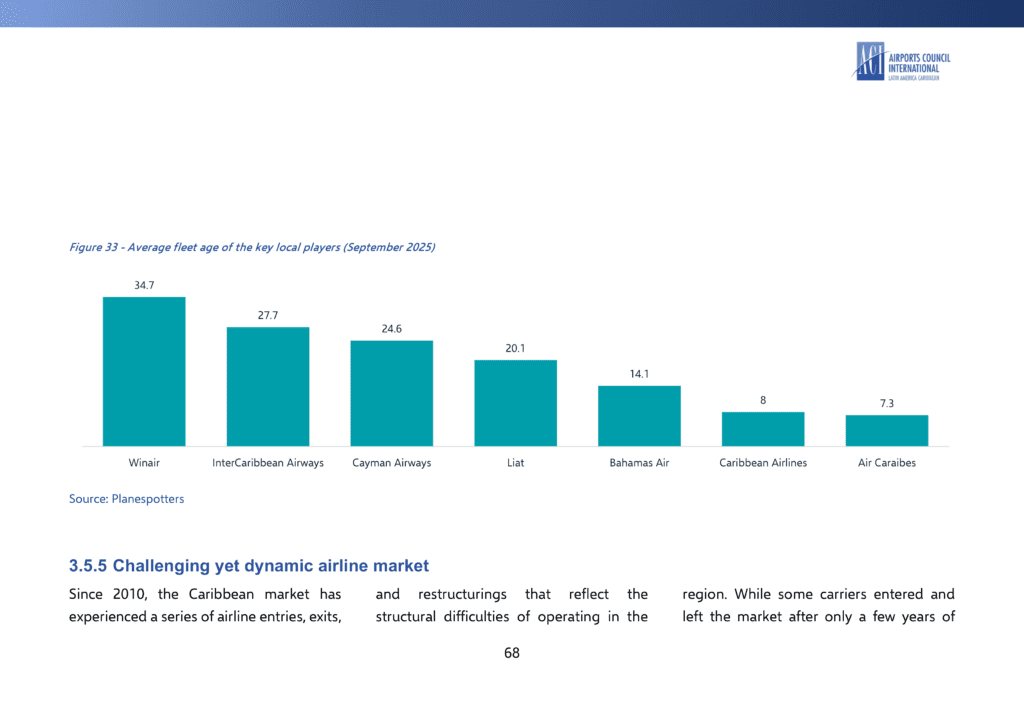

On top of this structural constraint, there is a fleet question. According to Planespotters data from September 2025 reproduced by NACO, the average fleet age of key local players varies significantly: 34.7 years for Winair, 27.7 years for InterCaribbean Airways, 24.6 years for Cayman Airways, 20.1 years for LIAT, 14.1 years for Bahamasair, 8 years for Caribbean Airlines, 7.3 years for Air Caraïbes. An older fleet most likely results in higher maintenance costs as parts deteriorate and repairs become more complex. Ground times also lengthen, and operational costs consequently tend to rise.

Average fleet age of key local players, September 2025. Air Caraïbes operates the youngest fleet at 7.3 years, ahead of Caribbean Airlines (8 years). Winair, at the other end, runs a fleet averaging 34.7 years. Source: Planespotters, NACO/ACI-LAC report, March 2026.

A regional reading: diversity as both fragility AND asset

The mapping drawn by NACO reveals a diversity of business models unusual for a region of this size. The report draws two complementary readings. On the one hand, this diversity reflects fragmentation: no Caribbean airline durably dominates the intra-regional market, preventing the emergence of economies of scale comparable to those observed in other island regions. On the other hand, this diversity of models is also an asset: it allows the region to serve markets of very different sizes, from very low-density links to higher-volume corridors, and reflects fine-grained adaptation to the heterogeneous needs of the region. The study’s recommendations (which we will explore in subsequent articles) aim precisely to better articulate this diversity rather than force it into uniformity.

Overview of the intra-Caribbean market by airline market share (seat capacity), excluding domestic, 2024. Source: Cirium, NACO Analytics, NACO/ACI-LAC report, March 2026.

Source : NACO (Netherlands Airport Consultants), The State of Air Connectivity in the Caribbean: A Renewed Vision for Progress, independent study commissioned by ACI-LAC, March 2026, 128 pages.