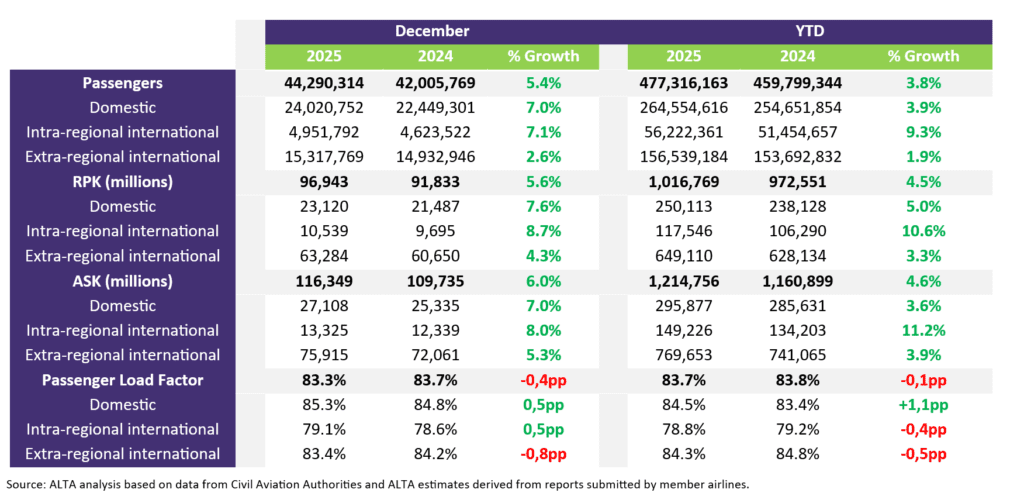

Latin America and the Caribbean closed 2025 with 477.3 million passengers, marking a 3.8% year-on-year increase and 17.5 million additional travelers compared to 2024. At first glance, the figure suggests steady consolidation rather than explosive expansion. Yet the data published by ALTA (Latin American and Caribbean Air Transport Association) reveals something more structural: a shift in the region’s aviation power dynamics.

Eighty-four percent of net growth came from domestic and intra-regional traffic. The center of gravity is no longer intercontinental recovery. It is internal consolidation. And within that movement, three countries stand out — Brazil, Argentina, and Panama — forming what increasingly resembles a new strategic triangle in regional aviation.

Brazil: The Demand Engine

Brazil remained the largest aviation market in Latin America in 2025, handling 129.6 million passengers, according to ALTA’s annual traffic report released in February 2026. The country alone contributed 11.2 million additional passengers year-on-year, representing a 9.4% increase — the largest net contribution in the region.

Two milestones underline Brazil’s structural weight. For the first time, domestic traffic surpassed 100 million passengers. International traffic also reached a historic high of 28.4 million passengers, growing 13.4% year-on-year.

What makes Brazil’s performance strategically significant is the inbound dimension. International tourist arrivals by air increased 33.2% in 2025, with Argentine visitors rising by 77%, according to figures cited in ALTA’s release. Air traffic between Brazil and Argentina expanded 29.7% year-on-year, accounting for roughly one-third of Brazil’s international traffic growth.

Brazil is no longer simply a large domestic market. It is acting as a regional demand magnet, strengthening South America’s internal corridors.

Argentina: The Acceleration Node

Argentina posted the highest percentage growth in the region in 2025. Total traffic reached 33.3 million passengers, up 13.2% year-on-year, equivalent to 3.9 million additional passengers.

Domestic traffic increased 9.1%, while international traffic surged 18.2%. The expansion of flight supply played a decisive role. According to ALTA’s data, traffic between Argentina and Brazil grew 38%, while routes to the Dominican Republic increased 93% and Colombia 28%.

This pattern reflects a context of greater market openness and expanded international connectivity. Argentina’s aviation growth in 2025 was not merely cyclical recovery — it was corridor-driven expansion. The country is emerging as a key accelerator of intra-LAC flows.

Panama: The Strategic Connector

Panama recorded nearly 21 million passengers in 2025, growing 9% year-on-year, equivalent to 1.7 million additional travelers. Unlike Brazil and Argentina, Panama’s strategic role lies less in volume and more in connectivity structure.

Origin–destination traffic between Panama and the United States totaled 4.63 million passengers in 2025, increasing 8.1% year-on-year. This is particularly notable given that total traffic between Latin America and the United States contracted by 0.3% during the same period, according to ALTA’s aggregated regional data.

Panama’s Tocumen hub continues to capture and redistribute flows even when broader continental traffic softens. It functions as a hinge between North and South America — a role reinforced by disciplined capacity management and consistent hub optimization.

Capacity Discipline and Market Balance

Beyond country performance, the structural health of the region stands out. ALTA reports that available seat kilometers (ASK) grew 4.6% in 2025, while revenue passenger kilometers (RPK) increased 4.5%. The regional load factor averaged 83.7% for the year.

Capacity expansion closely tracked demand growth. The total number of flights rose 2%, and seat capacity increased 3.1%, with an average of 160 seats per flight compared to 158 in 2024.

This alignment suggests a balanced market environment — neither oversupplied nor overheated. For airlines and airports, it reflects operational discipline rather than aggressive speculative expansion.

A Region Growing from Within

The defining feature of 2025 was not long-haul resurgence. It was regional reinforcement.

With 84% of net passenger growth coming from domestic and intra-regional operations, Latin America and the Caribbean are strengthening internal connectivity. Growth corridors such as Brazil–Argentina and Panama–United States illustrate that traffic is reorganizing around efficient regional flows rather than relying solely on transatlantic or transpacific demand.

Even markets with moderate or mixed results contribute to this structural picture. Mexico remained the second-largest market with 122.4 million passengers (+2.4%), while Colombia reached 57.5 million passengers (+1.7%), despite domestic softness in Bogotá. Peru recorded 28.5 million passengers (+5.9%), benefiting from expanded airport infrastructure in Lima. In the Caribbean, the Dominican Republic led growth with 19.6 million passengers (+3.1%), while Jamaica experienced a 7.7% decline, largely linked to operational disruptions following Hurricane Melissa in the fourth quarter.

These variations underscore a region in transition — diversified, corridor-driven, and increasingly intra-dependent.

Strategic Implications for 2026

The 3.8% regional growth rate confirms stability. But the deeper story lies in structural redistribution.

Brazil consolidates its position as the region’s demand engine. Argentina accelerates through liberalized connectivity and expanding international corridors. Panama strengthens its role as the north–south redistribution hub. Together, they form a triangular axis of influence shaping aviation flows across Latin America and the Caribbean.

If regulatory modernization and competitive frameworks continue to advance — as highlighted by ALTA CEO Peter Cerdá in the February 2026 statement — the region’s internally driven growth could accelerate further. The numbers tell a story of recovery. The corridors tell a story of reconfiguration. And in 2025, that reconfiguration placed Brazil, Argentina and Panama at the center of Latin America’s aviation power map.